Rates Just Got Smoked by Barn Burner Inflation Report

If it feels like there’s been an inordinate amount of focus on the Consumer Price Index (CPI) recently, today proved it was justified. It’s not hard to understand WHY this data should matter. After all, inflation is the biggest reason that rates moved higher at the pace seen in 2022/2023. From there, we only need to know that CPI is the biggest market mover among inflation reports and the focus quickly makes sense.

But that’s not the only reason that today was highly consequential. We were also in the midst of a bit of a correction in rates that took us from the best levels in 8 months to the worst levels in more than a month in the space of 2 days. In not so many words, the bond/rate market was essentially asking itself if it had been caught flat-footed heading into February. The jobs report on Friday, Feb 2nd said “yes!” Now today’s CPI data says “see?!”

So what happened?

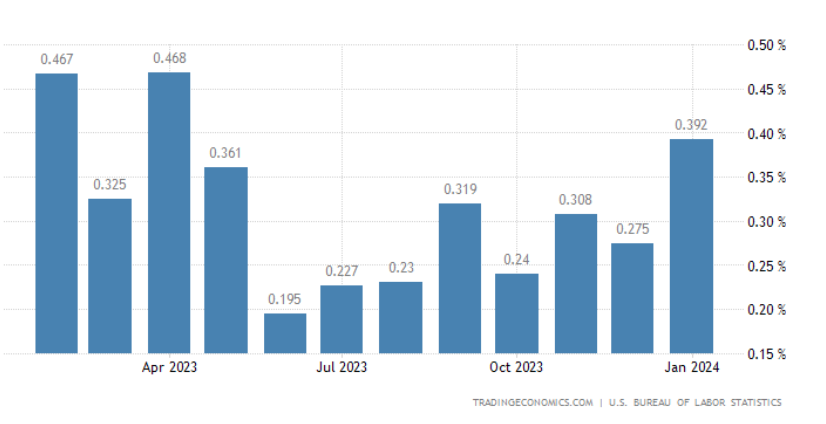

It doesn’t sound too interesting at face value. Core month-over-month inflation came in at 0.4% for January as opposed to the 0.3% seen last month. Markets expected it to hold steady, on average. Small monthly changes are very important when it comes to CPI–especially if those changes make a new argument about the momentum of inflation. Today’s report was in a unique position to make it look like that momentum had been cooling since last September. Instead, it now looks like it’s rising back toward levels from early 2023.

The bond market (which underlies mortgage rates) reacted immediately and forcefully when the numbers came out. Bonds continued to worsen as the day went on, leading many mortgage lenders to raise rates once or twice during the day. The net effect is an average 30yr fixed rate that moved well into the 7s after being in the high 6’s yesterday.